From Idea to Rule-Based Test

Instead of checking a few chart examples manually, define exact entry, exit and risk conditions. A rule-based backtest makes the same logic repeatable across dates and instruments.

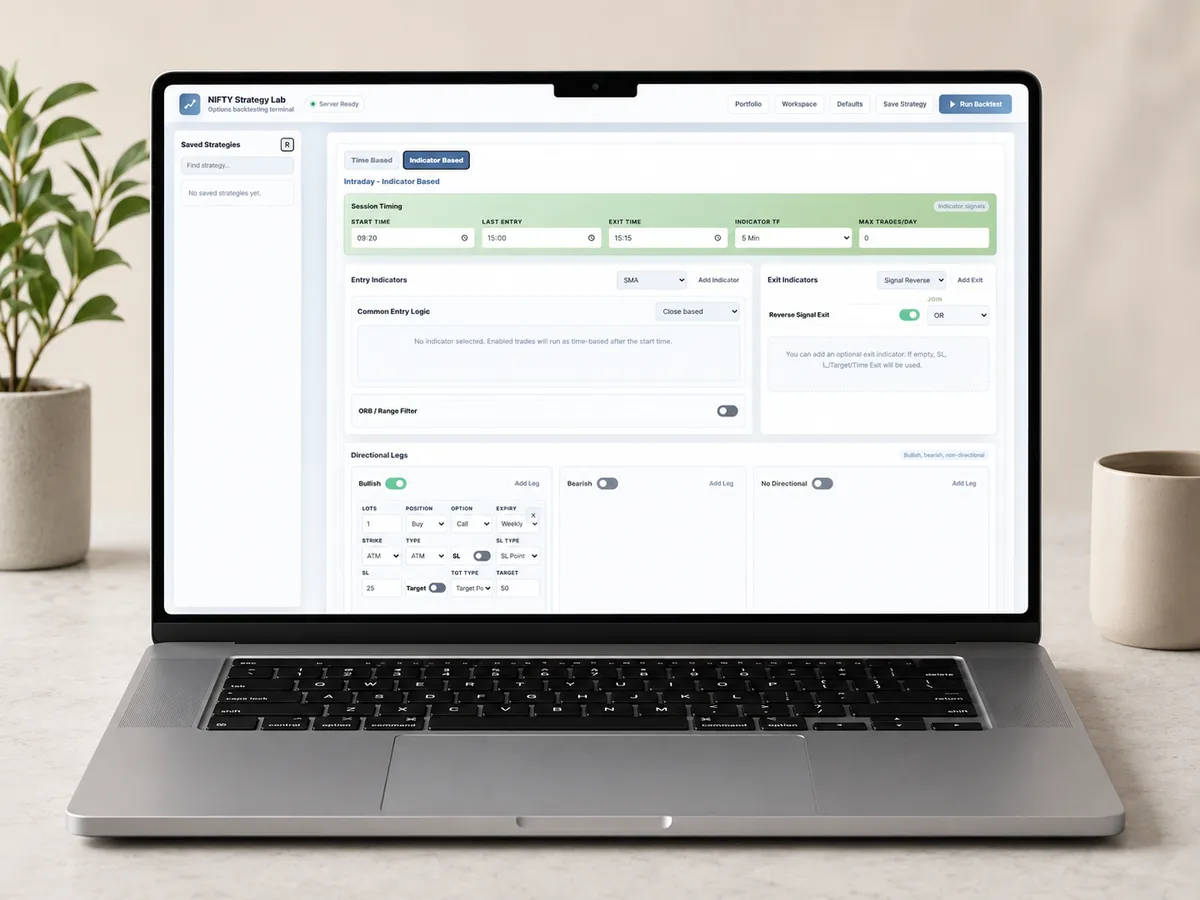

AlgoBacktest helps traders turn a strategy idea into a repeatable historical test. Build rules for options or stocks, run the backtest and study the report before using real capital.

Instead of checking a few chart examples manually, define exact entry, exit and risk conditions. A rule-based backtest makes the same logic repeatable across dates and instruments.

Use AlgoBacktest for NIFTY and SENSEX options workflows, stock intraday research, positional stock testing, strategy portfolios and stock screener scans.

Review P&L, drawdown, win rate, monthly returns, day-wise filters and executed trades. Backtesting is a research process, not a guarantee of future results.

AlgoBacktest is a historical backtesting and analytics platform. It does not provide trading calls, buy/sell recommendations or investment advice. Backtested performance does not guarantee future results.

It is testing a defined trading rule on historical data to understand how it would have behaved in the past.

Yes. AlgoBacktest supports options backtesting, stock backtesting and stock screener workflows.

No. Backtested performance does not guarantee future returns or live market outcomes.