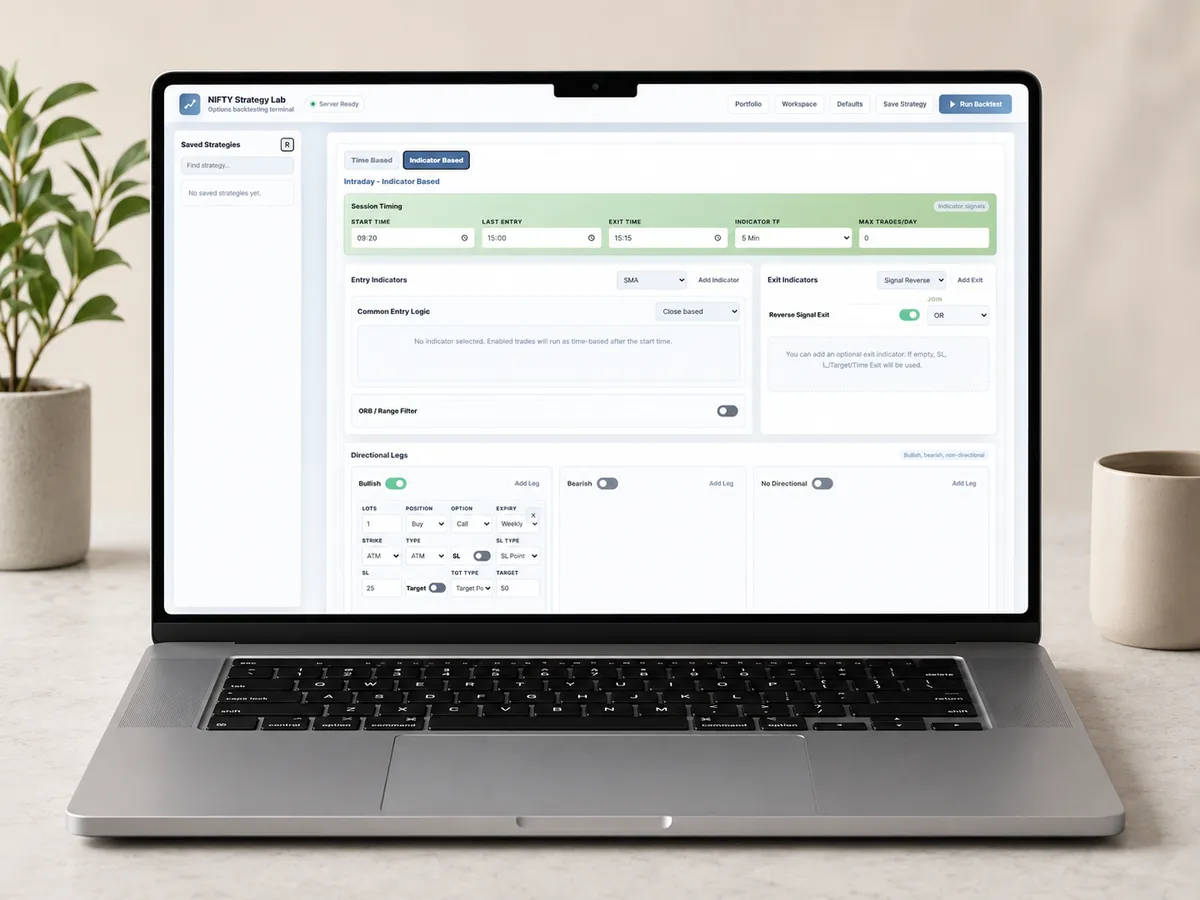

What You Can Test

- Multi-day strategy testing

- Indicator based positional entries

- Risk controls and re-entry support

- Monthly and day-wise performance reports

Test strategies that can stay open beyond intraday timing rules and review how they behave across longer historical periods.

Positional backtesting is useful when your idea depends on trend continuation, multi-day signals or wider risk assumptions.

Use defined entry, exit and risk conditions so the backtest is repeatable and not dependent on manual chart reading.

Review P&L, drawdown, monthly returns and executed trades after the positional run completes.

AlgoBacktest provides historical simulations only. Backtested performance has inherent limitations and does not guarantee future profits or similar live market results. Invest at your own risk.

Yes. Positional runs can evaluate strategies across multiple days instead of only one intraday session.

Yes, indicator based positional testing is supported based on plan access.